On Tuesday, October 10, Governor Phil Scott addressed attendees at the Promises Made, Promises Kept Conference, hosted by the Vermont Business Roundtable and Champlain College’s Center for Financial Literacy. His remarks and presentation follow.

GOVERNOR SCOTT: Good morning. Thank you to Lisa and the Vermont Business Roundtable for hosting this event—and to David for the inspiration to get together on this issue.

Today’s event begins another important conversation about my Administration’s commitment to affordability, economic growth, and protecting the most vulnerable. As I’m speaking, you’ll see some slides behind me, which will provide a visual for what I’m describing.

Let me start by giving you the three numbers that literally keep me up at night: Six, three, and one.

Every day when we wake up, on average, there are six fewer workers in our workforce, three fewer kids in our K through 12 education system, and nearly one baby born exposed to opiates. Every single day.

We must reverse these trends, and we can, if we face our challenges head-on and focus on expanding our workforce – because these are the people who buy homes, have families, utilize services, buy products and pay taxes.

All of us here in this room – state officials, business owners, community members, public employees and legislators – working together, can make the changes we need, if we agree on the goal and align every decision we make with achieving that goal. And, this is important, we also have to know exactly how we’re going to measure our progress.

On my first day in office, I issued an executive order outlining three simple principles that guide my Administration in every decision we make, as we work to reverse this “6-3-1” trends.

We ask ourselves:

- Does it grow the economy?

- Does it make Vermont more affordable?

- Does it protect the most vulnerable?

I’ve asked my cabinet, and I ask you, to consider focusing and prioritizing ideas that accomplish all three or, at a minimum, two-out-of-the three.

So, on [Slide 3] you’ll see the key indicators and specific metrics our team will be using to measure the progress we’re making on growing the economy, making Vermont more affordable and protecting the most vulnerable. Because, as someone famously said, “if you aren’t measuring it, you aren’t managing it.”

{kind=link}

More importantly, I’ve asked each agency and department to tell us the 3-5 things they can do over the next few years to move these indicators in the right direction, and we’re working on those things as we speak.

We’ve spent the first nine months of this new Administration rethinking our processes and focusing on having a clear strategic plan with measurable indicators and specific goals and tactics, which are all focused on reversing “6-3-1.”

Here’s one small, but powerful example:

As part of our PIVOT program to modernize state government and give more state employees the tools they need to support continuous improvement, we are training state employees in LEAN techniques. In the previous three years, about 300 hundred state employees were trained at a cost of about $650 per training day. In just four months this year, by prioritizing this work and leaning the training system itself, we’ve trained another 250+ state employees and we’re on track to have about a quarter of the workforce—or more—trained in LEAN by 2020.

I think everyone in this room is aware that, as a state, we literally can’t afford to keep doing things the way we’ve been doing them.

But here’s another way to look at it: If we want to protect the public investments we value, and if we want to make more of them, we must reverse the decline in our workforce.

The slow growth in Vermont’s economy, the decline in Vermont’s working-age population and tightening labor market conditions don’t allow us to be complacent. Everything we value and everything we aspire to do is at stake.

In August, I traveled to New York City with Treasurer Beth Pearce, members of my Cabinet, our state economist Jeff Carr and Chair of the Capital Debt Affordability Advisory Committee Dave Coates.

We were there to meet with three different rating agencies to discuss Vermont’s economy and whether Vermont was doing what was necessary to maintain its Triple A bond ratings.

I believe it’s critical to meet face-to-face with these rating agencies to ensure they know we understand our challenges. I also wanted to share my vision and goals to meet those challenges, and to underscore that my Administration continues – and is strengthening – the fiscal management the rating agencies have come to expect.

We made a few key points to those agencies.

First, we, as a state, make fiscal decisions around consensus economic forecasts.

Second, we maintain sufficient reserves.

Third, we honor the recommendations of our Capital Debt Affordability Advisory Committee about how much debt we can afford when we issue general obligation bonds each year.

Fourth, we roll up our sleeves and work together to address challenges.

And, finally, I detailed what we had done in the previous eight months to begin to reverse the trends of “6-3-1.”

We passed a truly historic budget that, for the first time in memory, didn’t add new taxes or fees, providing struggling Vermonters with a small amount of relief and an opportunity to keep more of what they earn.

We worked successfully to find efficiencies and $5 million in administrative savings across state government, on top of $28.5 million in rescissions in the Fiscal Year 2018 budget without deep program or workforce cuts.

With the deal we struck on the $35 million housing bond, we will begin to expand the stock of decent housing working families can afford – a resource we need to help attract families and young professionals to work and live in Vermont, and an investment that creates hundreds of trades jobs.

I asked for increased investment in early child care and learning for the same reason – and you can expect me to continue to advocate for a unified cradle-to-career education system that I believe can be the very best in the nation.

We also made investments in small business development centers, in regional microbusiness programs, and in economic development marketing.

Further, downtown tax credits were increased and six additional tax increment financing (TIF) districts were authorized to support development.

The rating agencies were convinced that we are taking the right proactive, aggressive approach.

But those ratings also came with some sobering, but not surprising, warnings that underscore the challenges we face in Vermont.

The fact is, Vermont’s economy is growing, but only slightly. And it’s growing more slowly than the average economic recovery across the U.S.

2017 statistics currently show a decline in overall jobs, tightening labor market conditions and personal income growth that is painfully slow for families.

When we compare Vermont to the other Triple A-rated states, we find ourselves consistently in the rear of the field – and I know, as a racecar driver, that’s not a good place to be.

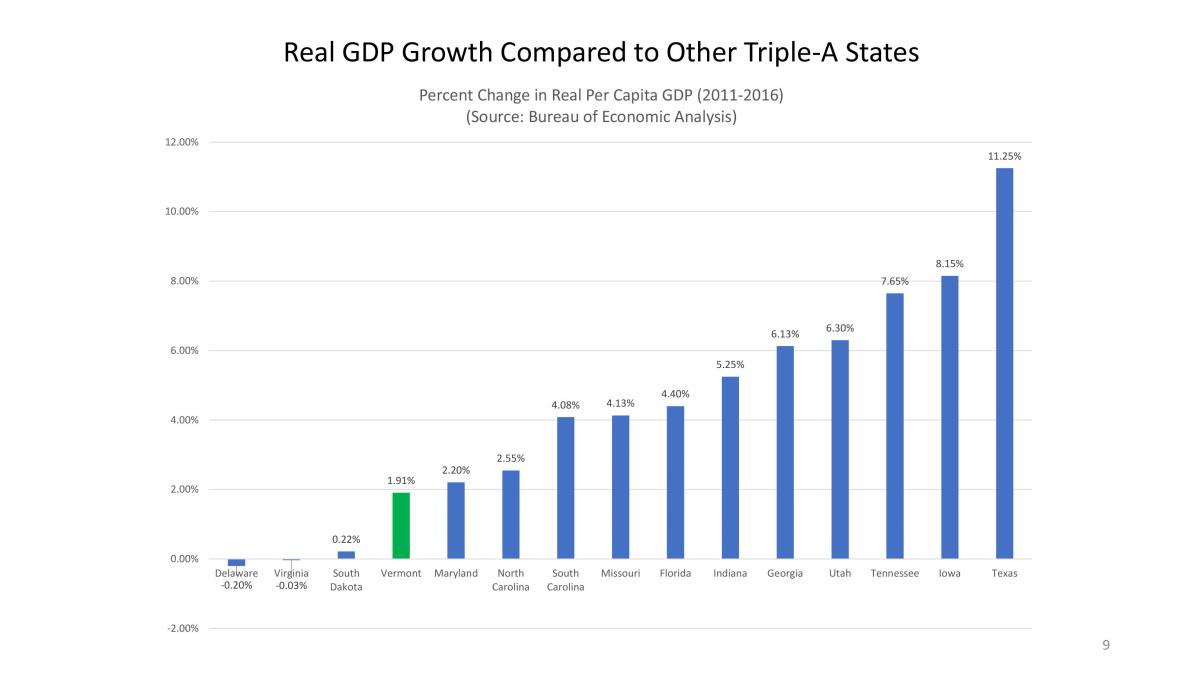

Vermont’s percent of change in real GDP growth per capita was the fourth lowest compared to the 15 other Triple A-rated states. That’s 1.91 percent in Vermont compared to 8.15 percent in Iowa and 11.25 percent in Texas. [See Slide 9]

{kind=link}

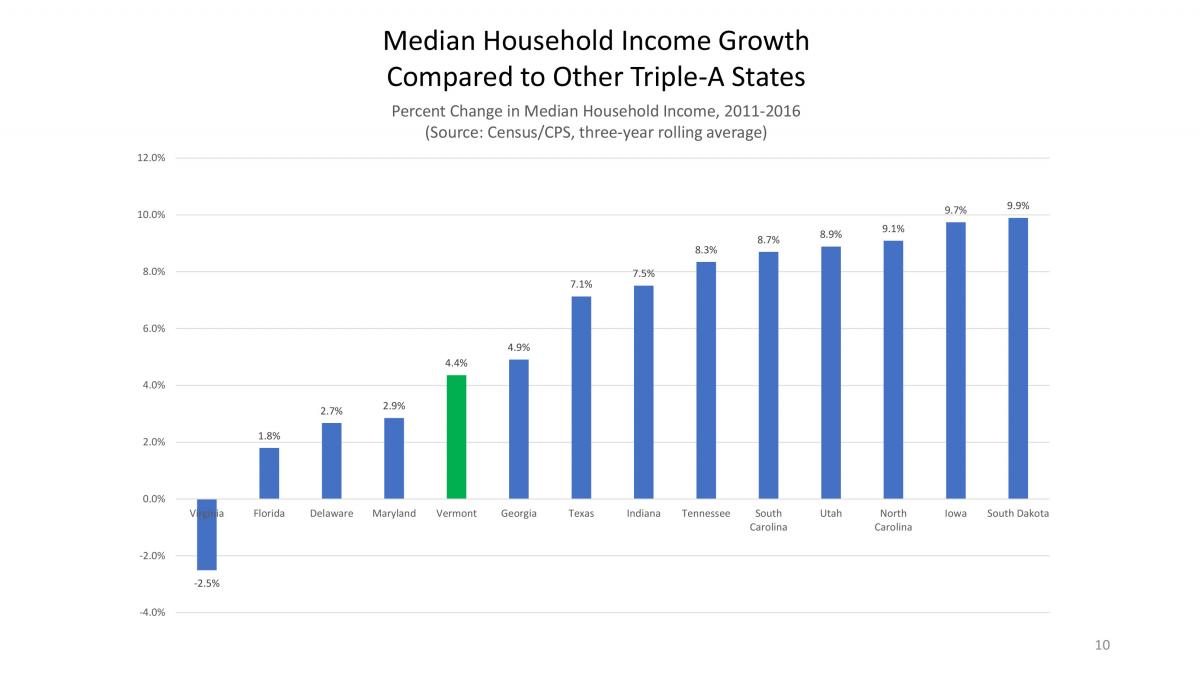

The median household income growth in Vermont is likewise well below that of other Triple A-rated states, with a percent change of only 4.4 percent between 2011 and 2016 compared to more than 8 percent growth in top-ranked Triple A states. [See Slide 10]

{kind=link}

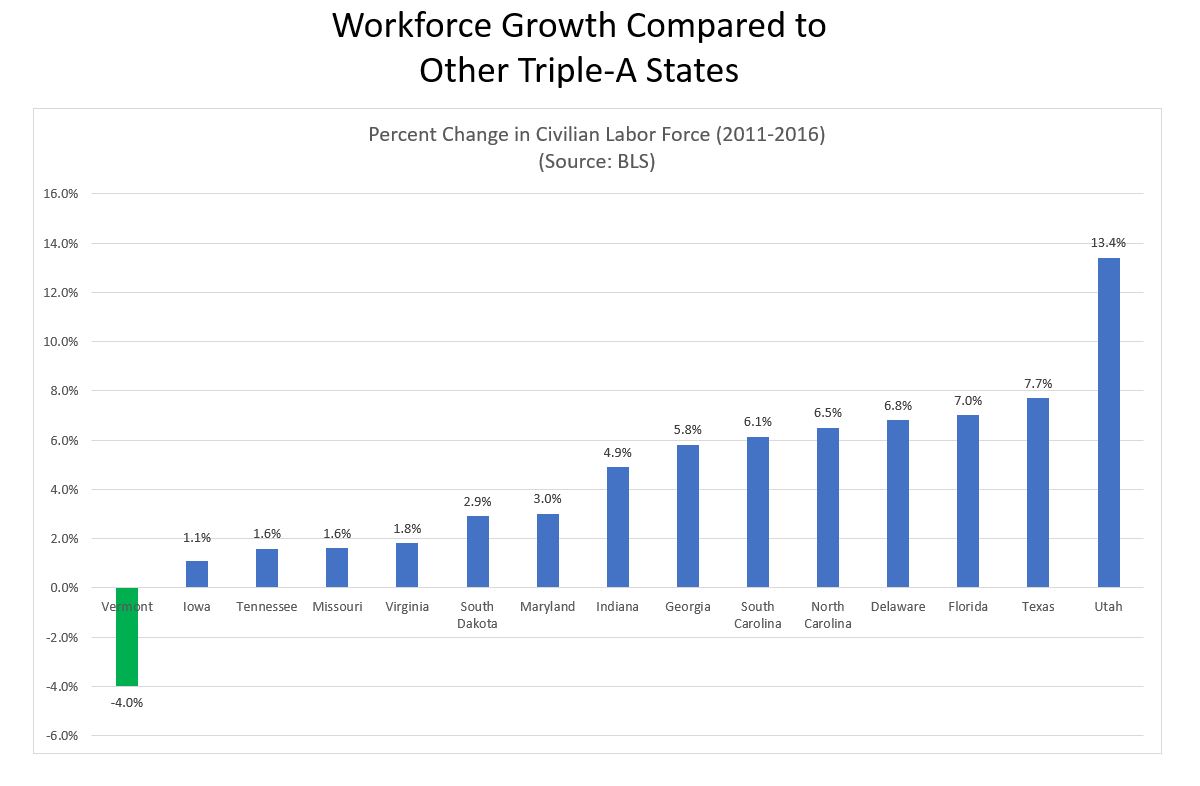

Finally – and, again, this is the biggest issue we face – Vermont’s workforce has dropped significantly below our Triple A peer states. In the last five calendar years, the percent change in our civilian labor force dropped to -4.4 percent, that’s negative 4.4 percent. [See Slide 11]

{kind=link}

Our workforce is shrinking and this demographic issue is clearly of concern to the rating agencies, to me and my team. Reversing it should be the top priority of every elected official, regardless of party or philosophy.

We must grow our working-age population and increase the size of our workforce in order to expand our tax base and invest in our future.

To illustrate our population and demographics crisis in a different way, Vermont has 25,000 fewer Vermonters aged 20 and under than we did in the year 2000.

We now have 60,000 more Vermonters over the age of 65 than we did in that same year.

We also have the second oldest population in the country.

And for the next decade – if we do nothing – this demographic trend is expected to continue with our population share over 65 expected to grow at a faster rate than the U.S. as a whole.

Of equal concern to the rating agencies was Vermont’s debt profile. Thanks to the work of Treasurer Pearce, Dave Coates and the rest of the Capital Debt Affordability Advisory Committee, Vermont is noted for its sound debt management.

Despite that management, our demographics are working against us in this area too.

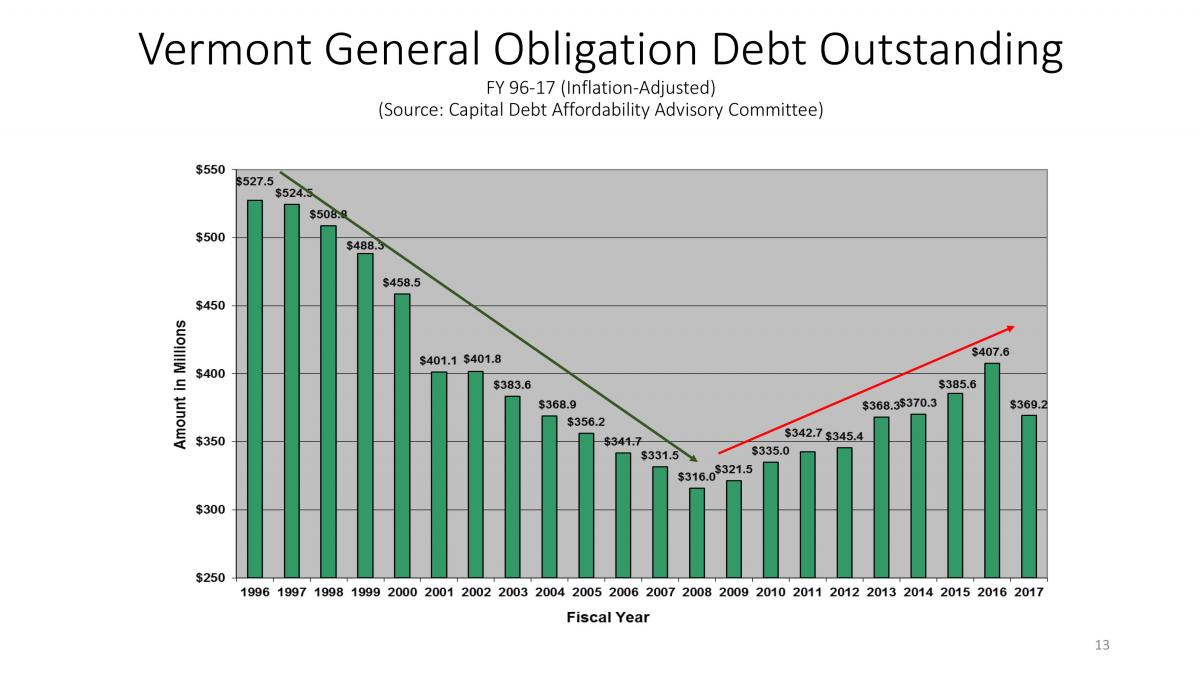

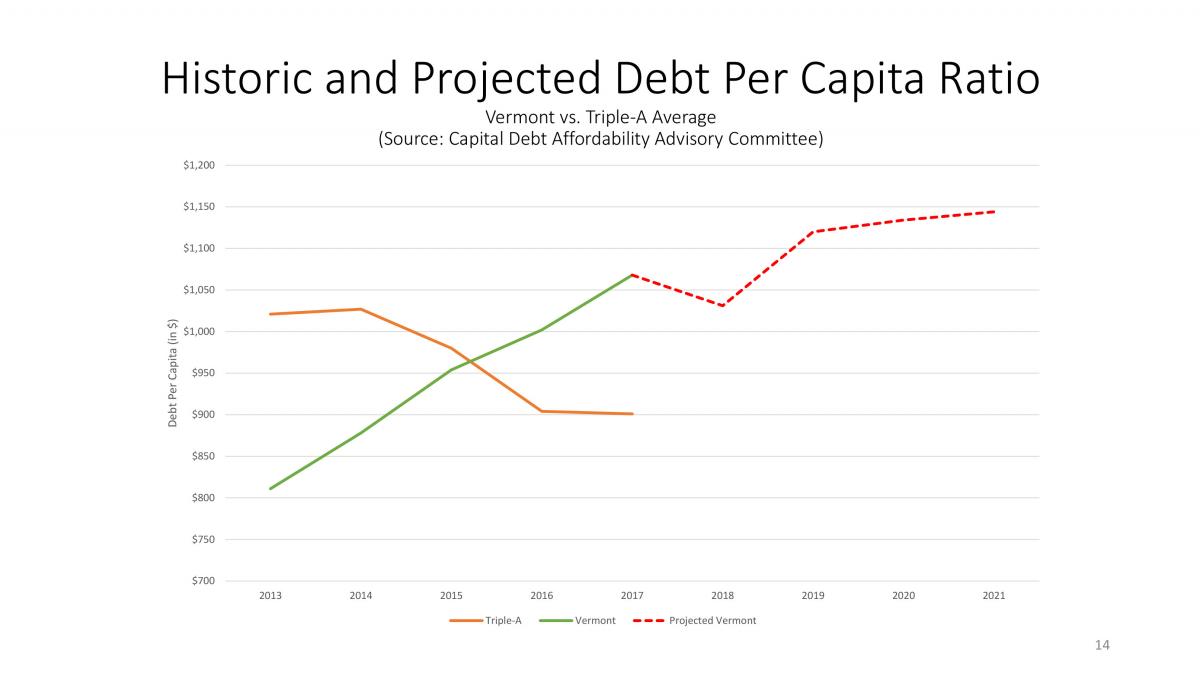

While we experienced a steady decline in our general obligation debt from the mid-90s to 2008, our debt obligations are growing while our population is essentially stagnant and actually slightly declining. [See Slide 13]

{kind=link}

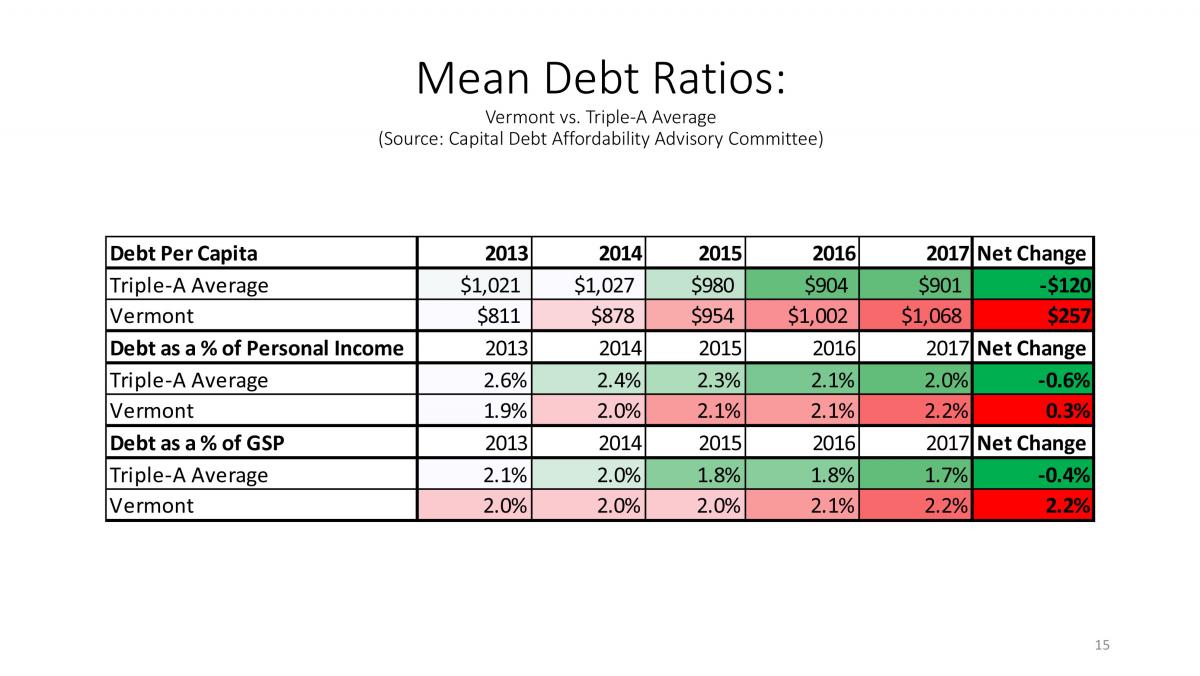

While the average debt-per-person declined by $120 since 2013 in other Triple A states, Vermont’s debt per capita rose by $257 during the same period, and is projected to continue to grow. [See Slide 14]

{kind=link}

Similar trends are apparent in the 0.3 percent increase in Vermont’s debt as a percentage of personal income. [See Slide 15]

{kind=link}

Vermont’s debt as a percentage of Gross State Product increased to 2.2 percent, while the Triple A average declined by 0.4 percent.

The point is Vermont is moving in the wrong direction in comparison to our peer Triple A-rated states. The rating agencies are monitoring these trends and we need to address them.

While we work to expand our workforce, decreasing individual tax burdens – including the debt load Vermonters bear now – is essential.

Finally, and what brings us together today, is the third economic caution from Wall Street: Vermont’s above average pension liabilities.

The difference between the money we set aside to pay retirement benefits to dedicated public employees is much less than the benefit the State has promised to pay them.

To the State’s credit, we have worked with the beneficiaries of the state and teachers’ retirement systems to negotiate changes in benefits, contributions and actuarial calculations. Market losses and other factors, however, have not allowed us to keep pace with our obligations.

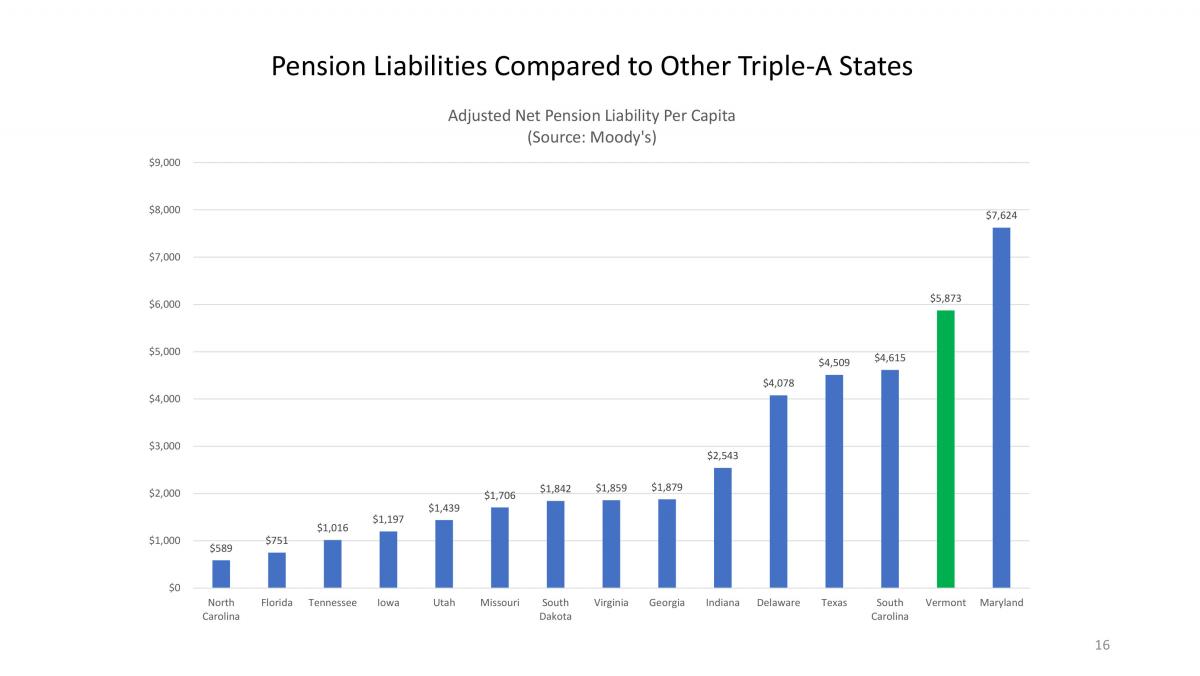

Vermont’s pension liabilities per capita are the second highest among Triple A-rated states at $5,873 per capita – topped only by Maryland. [See Slide 16]

{kind=link}

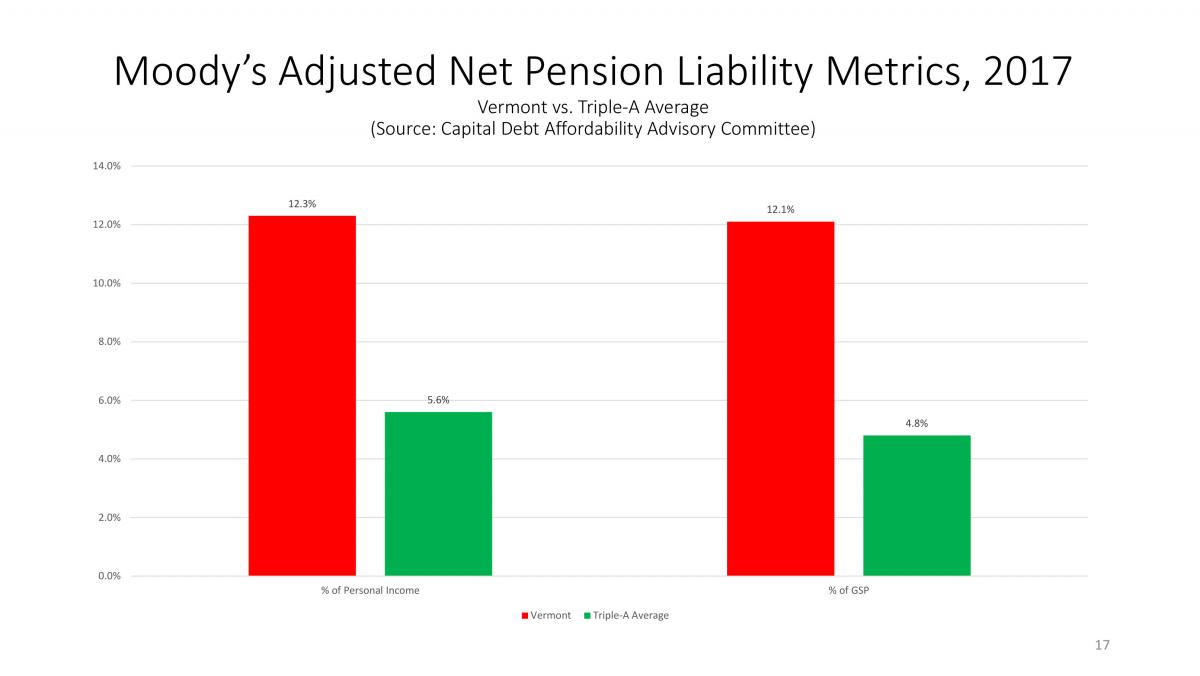

Our net pension liabilities as a percentage of personal income and Gross State Product are more than double the average of other peer Triple A-rated states. [See Slide 17]

{kind=link}

While we continue to struggle to fund our existing retirement plans, which will be much easier when we start growing the private sector workforce again, we must start the same conversation about whether maintaining the approach of the past is the right direction for our future.

We need to take the same pause with these plans as we have with taxes, fees and property tax rates, and think about what we are doing because we’re in a hole and we need to stop digging so we can build our way out.

I would describe myself as a realistic, pragmatic, optimistic Vermonter. I know we can – and we must – deal with these issues and reverse these trends.

But we, as a government, must find workable solutions with a greater sense of urgency and a greater focus than ever before.

I am grateful to everyone in this room who took the time to be here today to have the tough conversation that we must have, as Vermonters, with Vermonters.

By being here, you’ve shown you’re willing to listen and I hope today’s discussion will help us all pull in the same direction. Because when we do, the result will be powerful.

I hope you have a very productive and informative day.

Thank you.

END

Governor Scott's full presentation can be viewed by clicking here.

###